Hand Wringing In The IT Space Needs Company By Company Analysis

Today’s mixed report that the US labor market added more than a quarter million jobs but had unemployment rise should indicate that some sectors will maintain historical demand, while others will suffer downsizing driven by market conditions. In my view, the 18 month long stint for easy debt financing environment is the real culprit for specific types of layoffs. These layoffs involve companies that overestimated demand peaks lasting well into next year (or needed demand to extend that far into the future) and over hired to avoid an opportunity cost in a historically hot consumer market.

IT professionals should be as cautious as any other group about their respective sector and subsectors strength. But, no more nervous than other groups and, perhaps, a bit more optimistic even.

Despite the recent push for RTO, my suspicion is that everyone whose worth a decent salary still has leverage in their own way provided that they know the inner workings of their industry.

Analyzing Value Internally

Whose going to churn that data into a workable language model?

Whose going to automate those Jira tickets?

These tasks will certainly not fall on the 250k Data Scientist whose position may be more questionable than the 70 to130k professional quietly providing value in a mostly low-key way.

For instance, those individuals that work on products that involve business to business transactions, like Salesforce, could be in a better position than any product that is discretionary, like a Peloton bike or a website linked to travel. For some, it would be tempting to bucket an iPhone purchase in the discretionary category, but this purchase is on par with a house or car payment, which makes for a mutually reinforcing relationship between Apple and Samsung with all sorts of Telecom providers. In other words, those employees are fine since they basically work for a utility indirectly.

We have reason to be calm when we note where the layoffs are taking place. Remember, the IT sector, which is enormous, intersects with many industries but suffers from too much of an obsession with FAANG and FAANG-like companies. This skews our reasoning. Start-ups, like publicly traded companies, are very much subject to debt market conditions dictated by high or low fed interest rates.

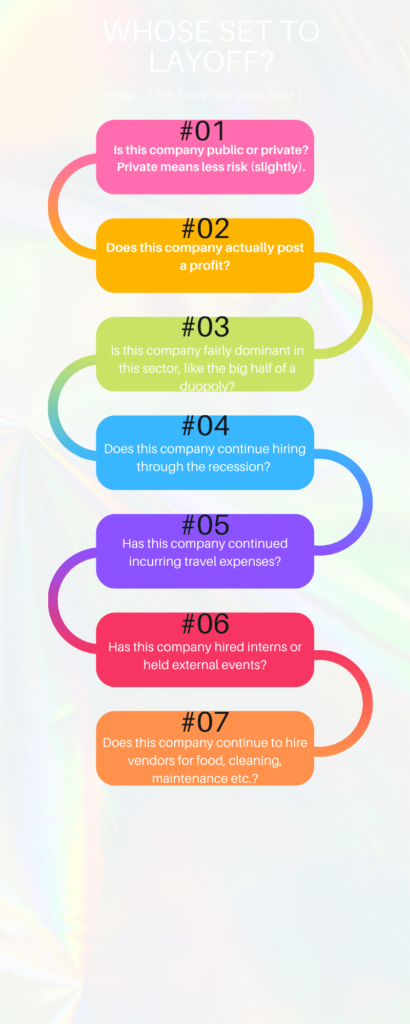

How I Think About Companies? After Step 1, Add 1 For Max Risk Score Of 6 For Layoffs:

Amazon Layoffs

In a non-exhaustive way, I think we can look at the most recent high profile layoffs with a grain of salt. With regards to Amazon, both IT services and deliveries had extreme usage entirely linked to discretionary funds made available through WFH. The same holds for all FAANG entities.

Meta Hiring Freeze

Meta is currently caught up in what amounts to investor fraud over usage numbers. Metaverse offerings have flopped because the market/social conditions no longer favor remote activities which also makes for even lower tolerance for the brittle technologies underlying them. In context, whereas Meta was once aligned with corporate ambitions to know everything about consumers, now they’re not aligned with a corporate pushback on remote work. We’re regressing back to 2019, essentially. Put another way, Meta’s ambition to have everyone stuck on a home-based VR set doesn’t advance corporate interests like its invasive advertising did a decade ago.

Never Profitable Start-Ups

As for Lyft, Uber and Twitter, they were all suffering from years of debt financed growth with no real clarity on future revenue or profitability. If anything, Twitter investors were basically subsidized by the recent Elon Musk purchase. Put another way, those positions were subsidized by investors who could not cash out. Now they have and those individuals must be let go from someone whose recovering acquiring an overprized asset.

Golden Parachutes

An overvalued C-Suite presence is always a fixture in start-ups, big and small. In 2 of those 3 companies, their C-Suite was constantly sued over sociopathic behavior. Wage theft. Liability. You name it, they got sued over it.

The business case for Lyft, Uber – despite their ubiquity – is weak since neither has ever accomplished the scale of user adoption needed to justify the investor expense. Therefore, in a financing environment that is levels more expensive than just a few months ago, these two entities would logically need to cut expenses just to service existing debt. The same applies for dozens of over-leveraged publicly traded companies. Too many IT companies are financed on the promise, not evidence, of profitability. Their visibility is just function of funny money too.

My point is specifics matter. Look under the hood because no one is going to do it for you. Personally, I’m tired of companies acting broke when they’re not and rich when they’re in debt.